Datafiles Jul 21

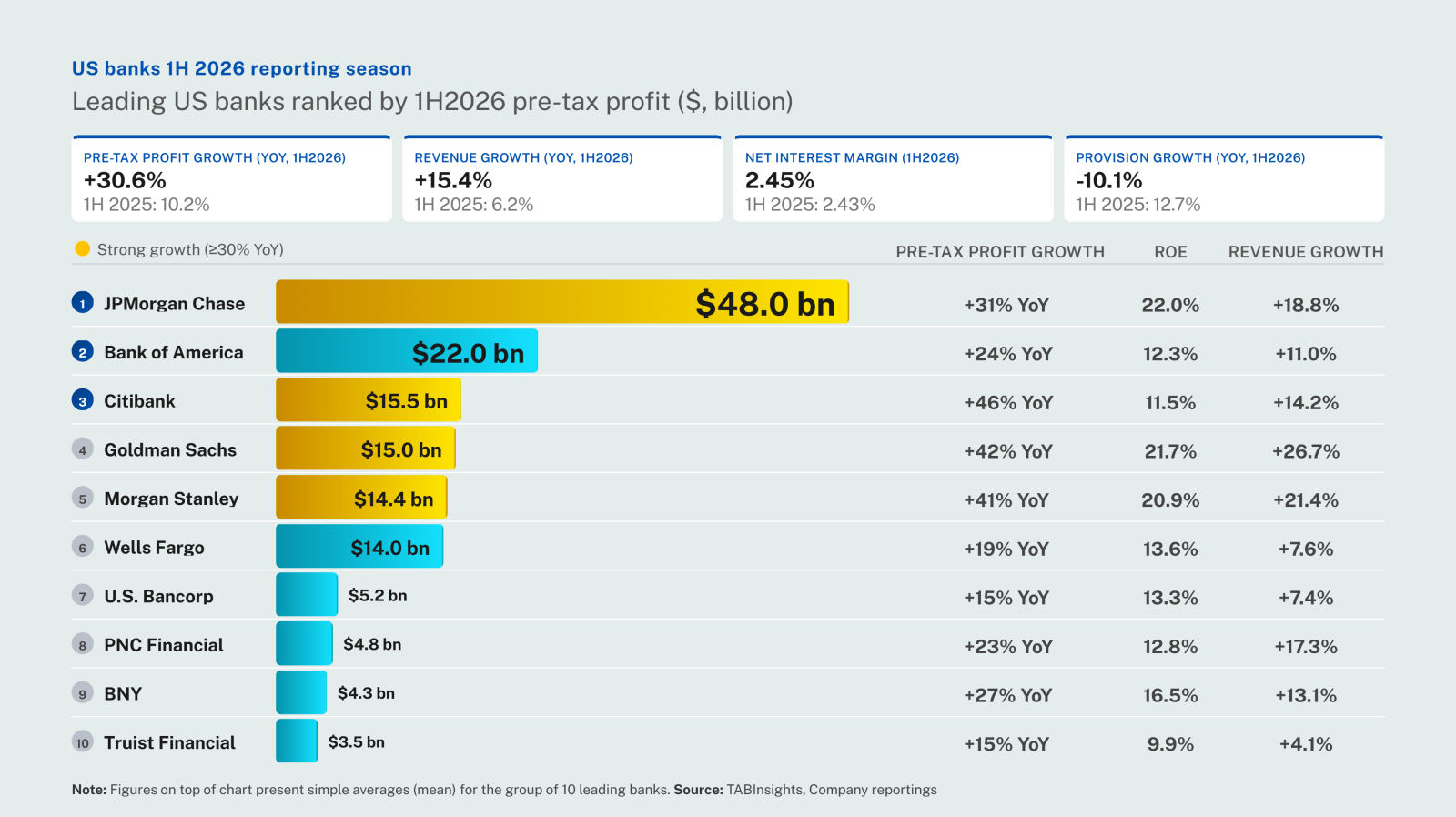

Robust capital markets activity and lower credit provisions lifted first-half earnings at leading US banks, but gains were concentrated among the largest, most diversified institutions. JPMorgan Chase led the group in absolute pre-tax profit, while limited margin expansion and slower revenue growth at regional lenders exposed a widening earnings divide.

.png)

.png)